Does 2024 promise better impact accounting?

The end of the fiscal year is undeniably stressful for everyone. Accountants and CFOs are under the cosh. Business owners, leaders, and employees alike are stretched thin, striving to hit targets at the last minute, pulling the right data, and making sure all the accounting i’s are dotted and t’s are crossed.

Despite the nature of this mandatory process, we endure it for a simple reason – the numbers represent a comprehensive narrative of the past 12 months, revealing successes, shortcomings, opportunities, risks, and areas for change.

It forms the bedrock upon which the strategy for the upcoming year is crafted and the previous years tested, eliminating the guesswork that would prevail in its absence.

Yet, when it comes to sustainability or impact reporting, limited data, unsystematic processes, and guesswork are worryingly common. The absence of a standardised framework for accurate impact accounting leaves businesses with well-intentioned but incomplete efforts. It’s all too easy to be unknowingly underperforming, and when the aftermath of that catches up with you, the effects can be devastating to your business and the wider communities you impact.

What’s the solution?

There is a renewed energy for developing standardised practices in impact accounting. The International Foundation for Valuing Impacts (IFVI) launched in 2022, growing out of the Impact Weighted Accounts Project at Harvard Business School. Early this year, in collaboration with the Value Balancing Alliance (VBA), they launched the exposure draft of the Conceptual Framework for Impact Accounting.

While it’s not new news, as the methodology builds on years of work through some of the key impact practice standards setters, it’s a good sign we’re taking steps in the right direction towards developing one common impact accounting methodology for the public good.

As this practice continues to develop, the transformative effects on businesses will see them able to assess their social and environmental impacts in connection with their financial accounts and make more informed business decisions based on their true value and cost. This will enable them to transparently and confidently showcase their impact as well as their profitability, building trust with stakeholders and providing a roadmap for sustained positive change.

It sounds like a necessary shift, so why aren’t we there yet?

Financial data, quite simply, has a head start. While not easy, it is more straightforward to calculate and has a highly well-resourced, externally audited, and standardised accounting system in place. It benefits from having an immediate and continuous effect on the overall success of any business or organisation, so there is always a business imperative to get it done and get it right.

Impact accounting, despite the many years of work of those like SVI, Capitals Coalition, Impact Economy Foundation, and IMP, is still in its infancy. There is still much discussion on what to include in impact accounts. There is much professional judgement to be made.

There is a need to deal with subjective wellbeing and value, as well as impacts from multiple perspectives, effect on the business itself, but more importantly, impact on those most affected, wider communities, staff, families, and the environment to consider.

Whilst your impact accounts will end up with numerical counts of impacts and values, the practice to get there is far more qualitative. Impact encompasses changes in dimensions of people’s wellbeing or alterations in the condition of the natural environment, with myriad variations and nuances. Each organisation faces unique challenges and opportunities, making the creation of a standardised approach more difficult.

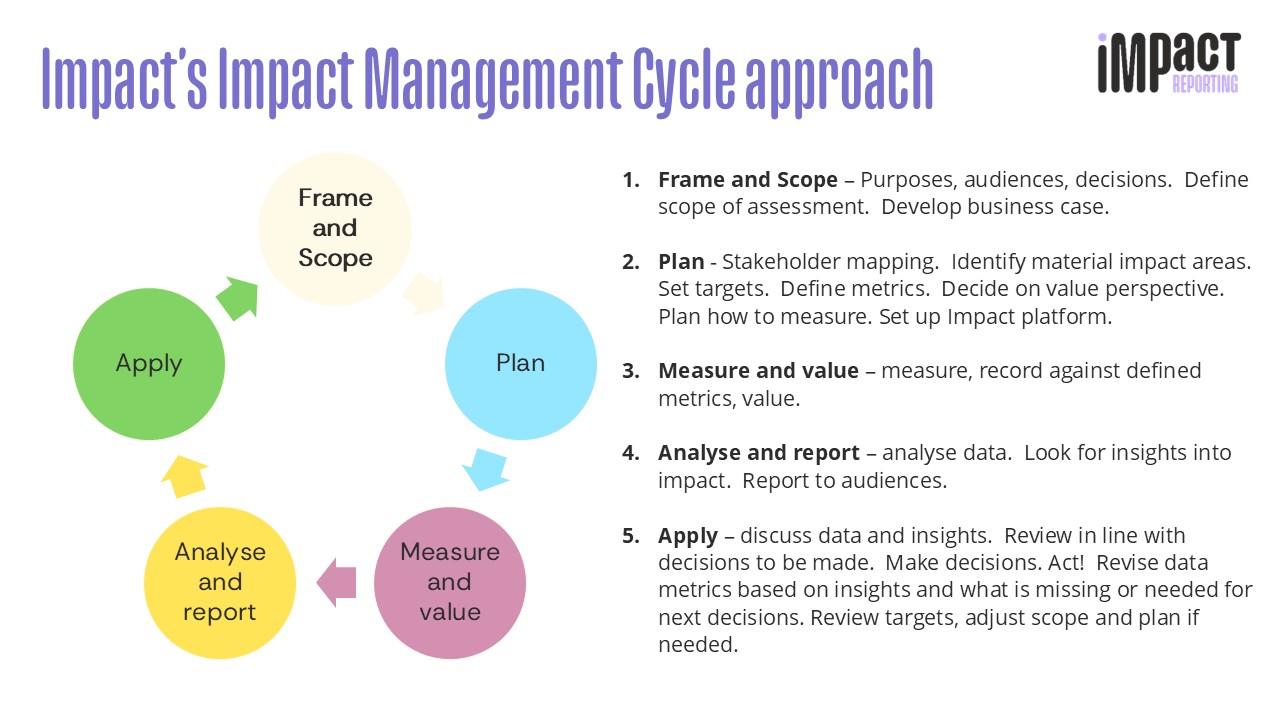

An agreement that value has been created is reliant on due process being followed. More than in financial reporting, impact accounting relies upon mapping to understand how value is created, who for, at what point to actually value it, and from whose perspective.

This includes such fundamental aspects of practice as impact pathways and impact materiality, monetary valuation, counterfactual and attribution. And most importantly, the voice of those most affected. All are aspects of practice used to take positive steps to quantify the unquantifiable and bring visibility to value.

The conceptual framework for impact accounting covers these key aspects in detail, some of which we highlight here:

Impact pathways

An impact pathway maps out the different causal relationships that lead from an activity to the impact that it has. The pathway will map out impact drivers, inputs, activities and outputs and how they lead to outcomes and impact. This helps impact metrics become more meaningful by assessing whether they indicate the outcome and impact has happened, rather than just counting whether an activity or output has happened.

Impact materiality

Impact materiality requires assessing the relative importance or worth of the different impacts primarily from the perspective of the affected person or people. This will be an iterative and ongoing process based on the level and completeness of the data available. Deciding what to include or exclude from accounts has a direct impact on the decisions made off the back of the accounts. It is a fundamental part of impact practice that continues to develop in understanding and quality.

Stakeholder engagement

Understanding who the people affected by your activities are is central to understanding your impact. Common stakeholder groups outlined in the conceptual framework are authorities, including central banks, governments, regulators, and supervisors, business partners, civil society, employees, other workers, trade unions, consumers, customers, end-users, existing and potential investors, lenders, and other creditors, local communities and vulnerable groups, non-governmental organisations, and suppliers.

While the shift towards better impact accounting is not guaranteed for 2024, the current landscape reflects significant strides in the right direction.

Esteemed organisations such as the International Foundation for Valuing Impacts (IFVI), and the Value Balancing Alliance (VBA), with the backing of Harvard Business School (HBS) through the Impact Weighted Accounts Project, inspire confidence that a common impact accounting methodology is on the horizon.

For more resources on achieving better impact management, stay up-to-date with our insights here. If you’d like to learn more about Impact Reporting, schedule a demo or contact our team at 0161 532 4752.