Guiding Principles to Follow in Social Value

Build trust, make better decisions, and amplify your impact with a principles-led approach.

Good social value practice starts with clarity, not complexity. This guide dives into the core Principles of Social Value and shows how they help you measure, manage and report what truly matters for people, communities and the planet.

Contents

- The 8 principles of social value

- How to use Social Value Principles to guide your social value

- The Impact measurement and management (IMM) approach

- Social Return on Investment (SROI)

- Sustainability, ESG and global reporting frameworks

- Other frameworks to be aware of

- Reflection and resources: 10 Impact questions

Why principles matter more than ever

Social value isn’t just another reporting requirement – it’s a way of thinking that shapes how organisations act, learn and improve. At its heart are a set of guiding principles that make your social value practice credible, transparent and useful for the people and places you aim to benefit.

In this guide, we unpack the guiding principles to follow in social value – from involving stakeholders and valuing what matters, to being transparent and responsive. You’ll learn what each principle means in practice, how they fit into real-world impact measurement and management, and why applying them thoughtfully is key to better decision-making, stronger accountability and greater trust with stakeholders.

Whether you’re new to social value or looking to deepen your existing practice, this guide equips you with a clear framework and practical insights to help you do social value well.

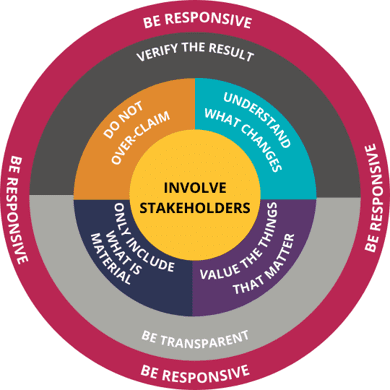

The 8 Principles of Social Value

The Social Value Principles are basic social accounting principles that guide good practice. They can be thought of as the basic underpinning building blocks to abide by when doing social value accounting. The 8 principles are:

Principle 1. Involve stakeholders

Inform what gets measured and how this is measured and valued in an account of social value by involving stakeholders.

Ask: Are we involving the right people in defining our outcomes? Who is most affected by our activities?

Principle 2. Understand what changes

Focus on outcomes, not just outputs. Articulate how change is created and evaluate this through evidence gathered, recognising positive and negative changes as well as those that are intended and unintended.

Ask: Are we clear on the changes we are making for people and planet, not just the activities we deliver?

3. Value what matters

Making decisions about allocating resources between different options needs to recognise the values of stakeholders. Value refers to the relative importance of different outcomes. It is informed by stakeholders’ preferences.

Ask: Are we giving weight to the outcomes that matter most to our stakeholders?

Principle 4. Only include what is material

Determine what information and evidence must be included in the accounts to give a true and fair picture, such that stakeholders can draw reasonable conclusions about impact.

Ask: Are we clear about what impact information matters, to whom, and why we are including or excluding this from our impact accounts?

Principle 5. Do not overclaim

Only claim the value that activities are responsible for creating.

Ask: Are we sure all of the impact we claiming is down to us? Would it have happened anyway? Was it caused by something else?

Principle 6. Be transparent

Demonstrate the basis on which the analysis may be considered accurate and honest, and show that it will be reported to and discussed with stakeholders.

Ask: Can a reader understand our data gathering and analysis methods, who was involved in the process, and any limitations or risks with our approach?

Principle 7. Verify the result

Ensure appropriate verification of results in line with the decisions being supported. In cases where results are being reported to external audiences and/or are supporting significant decisions, independent assurance is required.

Ask: Do we have systems for validating our data and findings?

Principle 8. Be responsive

Optimise the impacts on wellbeing of all materially affected stakeholders through decision making that is timely and supported by appropriate accounting and reporting.

Ask: How can we use this information in our decision making to improve our impact (make more good, make less bad)?

How to use Social Value Principles to guide your social value

At Impact Reporting, the Social Value Principles guide our practice, and we use these as a guide to support the practice of our clients. We see social value and impact management practice as iterative and continuous, with an aim to always be looking for ways to improve our impact, and to improve our social value and impact management practice. This means we won’t be purist or dogmatic about applying these principles, or any other practice frameworks, standards, or guidance, but will work with our clients to advise and guide on how to take next steps to improve in line with best practice standards as they stand.

Helpful resources

- What are the Principles of Social Value? – Social Value UK – SVUK page on the Principles of Social Value including:

- Principles of Social Value overview: Principles of Social Value (socialvalueuk.org)

- Purpose of the Principles overview: The Purpose of the Principles of Social Value and the SVI Standards (socialvalueuk.org)

- Social value assessment guide: https://www.socialvalueint.org/self-assessment-tool

Impact measurement and management (IMM) approach

Impact measurement and management (IMM) has its roots in the world of impact investing, where investors needed reliable ways to assess and compare the impact of their capital. Over time, the practice has expanded across sectors — especially where there’s a growing demand to show how organisations are responding to environmental and social change.

Today, IMM plays a critical role in helping organisations track, learn from, and improve the outcomes they create. This isn’t just about satisfying funders or regulators, it’s about understanding how you’re helping or harming people and the planet, and what decisions can improve that balance.

The GIIN defines IMM as:

“Identifying and considering the positive and negative effects one’s business actions have on people and the planet, and then figuring out ways to mitigate the negative and maximise the positive in alignment with one’s goals. Impact measurement and management is iterative by nature.”

IMM is another term that can be a unifying umbrella for related areas of practice like CSR, ESG, sustainability, non-financial reporting, and social value. It is important to be clear in your own practice how you are using these terms, whilst accepting that there will likely be some cross over with how others are using and understanding them. From a technical perspective IMM refers to the practical implementation of systems and processes for measuring impact and then managing the results, ie. making decisions informed by the findings about your impact.

Looking at broader practice, IMM can be best implemented when embedded within sustainability commited organisational structures which, as outlined by the UNDP Impact Practice Standards, will include a strong Governance structure, lead by a well developed Strategy, and quality assured through Transparency in reporting and accounts.

The Impact Investing Institute adds:

“Impact measurement tells us if we are achieving that positive, material and additional change. Impact management requires effective measurement and monitoring — we need to know what to expect from investees, and how to report to investors.”

Beyond measurement: managing for impact

IMM is about more than collecting data. It includes:

- Using evidence to guide decisions

- Comparing performance against targets

- Reducing negative effects and increasing positive ones

- Embedding impact across your full cycle of planning, delivery, evaluation and learning

Organisations like Social Value UK, Kusif, UNDP and Capitals Coalition all describe this as part of a bigger mindset shift — sometimes called impact thinking, a learning culture, or transforming decision-making.

The publication of Social Value Principle 8: Be Responsive by Social Value International reflects this evolution, encouraging organisations not just to report on what happened, but to actively adapt and respond based on what they’ve learned.

The impact management norms

To bring consistency across frameworks, the Impact Management Project developed a set of global impact management norms, now supported by:

- Impact Management Platform – coordinating global guidance

- Impact Frontiers – advancing investor and practitioner collaboration

These resources offer a practical and widely recognised foundation for IMM.

5 Dimensions of Impact

The Impact Management Project defined five key dimensions to help assess and compare impact:

There are data categories under each dimension of impact that organisations can use as guidance for their own impact data gathering:

- What: Which outcomes will be experienced or are being experienced? For each outcome – Define outcome level experienced, whether positive or negative, intended or unintended, outcome threshold – threshold at which the outcome is positive below which the stakeholder (or planet) would consider it negative, the importance to the stakeholder (relative to the other outcomes), alignment to SDG target or other goal.

- Who: Stakeholders type, people or planet, and how underserved? Key characteristics (e.g. age, location, gender, income level, industry), geographical location and boundary, outcome level at baseline (the level of outcome being experienced before or otherwise to the intervention)

- How much: a measurable change, how many (scale), duration (how long), depth (degree of change)

- Contribution: at enterprise level and at investor level, what do we add in relation to what would have happened anyway, what can you reasonably take credit for (as an investor), the counterfactual for both depth and duration

- Risk: how can your impact turn out differently or worse than expected? Type of risk (9 types of impact risk: evidence, external, stakeholder participation, drop-off, efficiency, execution, alignment, endurance, unexpected impact), and level of risk (likelihood, severity)

The ABC of impact

This model helps classify an organisation’s intentions for impact. Are you trying to reduce harm? Provide clear benefit? Contribute to long-term solutions?

The definitions of ABC are:

A: ACT TO AVOID HARM

An organisations activities should at least be avoiding causing harm. This is achieved through identification of ways the organisation is or could cause harm to people or planet and aiming to improve the outcomes so they get nearer to the sustainable social or environmental threshold. This is a reasonable objective for performance that will achieve sustainability for the outcome within the period of action that the objective covers.

B. BENEFIT STAKEHOLDERS

The next step is to actively benefit affected stakeholders by not only avoiding harm, but taking action to maintain or improve wellbeing for groups of people or aspects of the planet, so that it is within the sustainable range established by the societal or ecological threshold.

C. CONTRIBUTE TO SOLUTIONS

Contributing to solutions means improving the wellbeing of the affected stakeholders, both people and planetary, so that the outcome moves from being unsustainable into being sustainable. In this case the unsustainable outcomes should not have been originally caused by the organisation or activities that are now contributing to the solution.

For an enterprise to classify as “C” based on an outcome, half or more of the enterprise’s stakeholders experiencing that outcome should otherwise have been underserved with regard to the outcome, and half or more of the enterprises’ business should be generating that outcome, as measured by the proportion of revenue (if the outcome is associated with products or services) or costs (if the outcome is associated with enterprise operations).

Two further classifications can be used:

D. DOES CAUSE HARM. For when an unsustainable outcome is not being improved

M. MAY CAUSE HARM. For when there is no performance information for an outcome.

To apply ABC classifications to impact objectives it is necessary to have a clear understanding of thresholds relating to the particular outcome in question.

Learn more here: https://impactfrontiers.org/norms/abc-of-enterprise-impact/

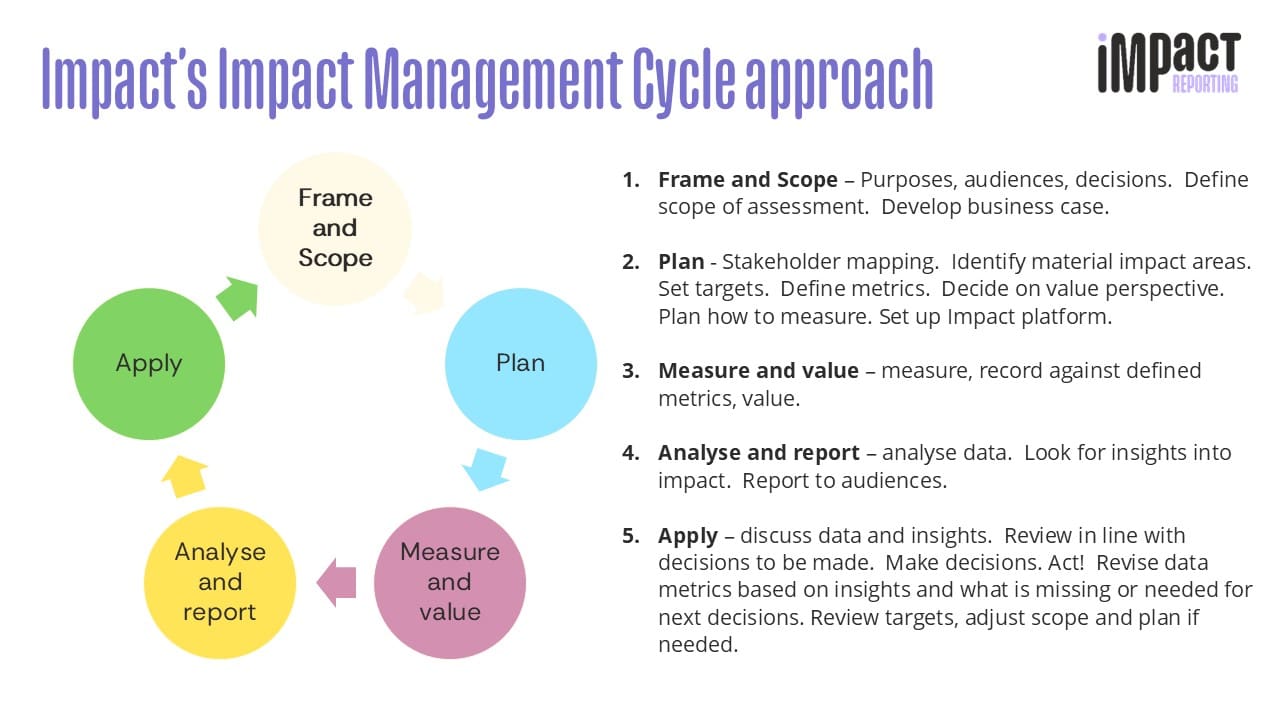

A practical cycle for managing impact – our approach

Impact management follows a cyclical process, similar to how you might manage a project, strategy or budget. The steps we follow at Impact are:

- Frame and scope – Define purpose, audience and boundaries. Develop your case for doing the work.

- Plan – Identify stakeholders, set targets, define metrics and decide how you’ll measure value.

- Measure and value – Collect and record the data.

- Analyse and report – Find insights. Share what you’ve learned.

- Apply – Use the data to make decisions. Adjust your approach, metrics and scope based on what you’ve learned.

This cycle builds on established guidance from Maximise Your Impact, Inspiring Impact, the BSI BS8950 standard, and the Green Book

Social Return on Investment (SROI)

Social Return on Investment (SROI) is a framework for accounting for social value. It applies the Social Value Principles in a structured way to help organisations understand, measure and value the social, environmental and economic outcomes of their work.

The SROI approach can be used to evaluate existing activities or to plan and forecast future impact.

The six stages of SROI

SROI follows a six-stage process:

- Establishing scope and identifying stakeholders: Define the boundaries of your analysis and identify who is affected by your work.

- Mapping outcomes: Develop a theory of change or impact map that shows the relationship between activities and intended results.

- Evidencing outcomes and giving them a value: Collect data to understand whether change has occurred, and assign a value to each outcome.

- Establishing impact: Adjust for factors such as deadweight, attribution and displacement to isolate the change your work is responsible for.

- Calculating the SROI: Compare the value of your outcomes to the cost of achieving them to generate a ratio (e.g. £5 of social value created for every £1 spent).

- Reporting, using and embedding: Share your findings and integrate the insights into strategy, operations and decision-making.

Proportionality and rigour

SROI is flexible. It can be undertaken to different levels of rigour, depending on the:

- Purpose of the analysis

- Intended audience

- Decisions the findings will inform

- Resources available (budget, time, data)

What matters most is that the core principles are followed — particularly involving stakeholders. This means:

- Stakeholder preferences must shape the definition and measurement of outcomes

- Valuations should reflect what matters to the people affected

- Materiality should be judged from the stakeholders’ point of view

Standards and guidance

Since the original SROI Guide was published, several supporting standards have been developed to help apply the Social Value Principles more consistently. These documents should be read and used together.

Some useful resources:

- Starting Out on SROI – Social Value UK: A practical introduction for those new to the methodology.

- Social Value Self Assessment Tool: A free interactive tool to assess your organisation’s current social value practice.

- Guide to SROI – Social Value International: The original step-by-step guidance on how to carry out an SROI analysis.

Sustainability, ESG and global reporting frameworks

As social value becomes more embedded in policy and business, it’s important to understand the wider ecosystem it operates within. Sustainability, ESG (Environmental, Social and Governance), and non-financial reporting frameworks each bring different priorities — but all are part of the broader movement toward transparency, accountability and long-term value.

This section gives you a high-level overview of key terms and standards that anyone working in social impact should be familiar with.

What is sustainability?

The modern definition of sustainability comes from the United Nations Brundtland Commission (1987):

“Meeting the needs of the present without compromising the ability of future generations to meet their own needs.”

It’s a guiding principle that connects environmental protection, social equity and economic resilience — the so-called triple bottom line.

The Sustainable Development Goals (SDGs)

In 2015, the United Nations launched the Sustainable Development Goals (SDGs) — 17 global goals designed to achieve a better and more sustainable future for all by 2030. They cover challenges such as poverty, health, education, gender equality, climate action and peace.

The SDGs are widely used by governments, funders and businesses as a shared reference point for their sustainability and impact commitments.

If you’re working in strategy or reporting, SDG Compass offers guidance on how to align your work to the goals and measure your contribution.

What is ESG?

ESG stands for Environmental, Social and Governance. It’s a way for organisations — especially in finance and investment — to evaluate risk and performance in non-financial areas.

ESG frameworks typically focus on inputs, activities and disclosures, such as:

- Environmental policies and carbon footprint

- Fair labour practices and human rights

- Governance structures and leadership ethics

Unlike social value or impact practice, ESG doesn’t usually track outcomes or ask how people’s lives have changed — but it does form the basis for many mandatory and voluntary reporting frameworks.

Reporting standards to be aware of

Whether you’re working in sustainability, impact, or social value, you’re likely to encounter some of the following reporting standards. These frameworks help organisations disclose their performance consistently and credibly.

GRI – Global Reporting Initiative

GRI Standards are among the most widely used for sustainability reporting. They cover environmental, social and economic impact.

- Universal Standards (apply to all organisations)

- Sector Standards (sector-specific impact guidance)

- Topic Standards (focused disclosures, e.g. on waste, water, or labour)

🔗 Short introduction to the GRI Standards (PDF)

ISSB – International Sustainability Standards Board

ISSB was created by the IFRS Foundation to develop global standards for sustainability disclosure. It brings together frameworks like SASB, TCFD and CDSB.

So far, it has published:

- IFRS S1 – General requirements

- IFRS S2 – Climate-related disclosures

Standards will continue to expand. While implementation is up to national jurisdictions, many organisations choose to align voluntarily.

SASB – Sustainability Accounting Standards Board

Now part of ISSB, SASB provides 77 sector-specific standards, helping organisations identify material sustainability issues relevant to their industry.

CSRD – Corporate Sustainability Reporting Directive

This EU directive requires companies to report using European Sustainability Reporting Standards (ESRS), developed by EFRAG.

- ESRS introduces double materiality — reporting both on:

- How a company affects people and the planet

- How sustainability issues affect the company

This approach aligns closely with the goals of impact management.

UK Sustainability Reporting Standards

The UK is developing its own approach to sustainability reporting in response to ISSB and CSRD. These standards are part of the broader Sustainability Disclosure Requirements (SDR), linked to the Mobilising Green Investment – Green Finance Strategy.

As of now, organisations in the UK often follow EU or international standards. Reporting expectations may evolve under future governments.

Other frameworks to be aware of

You don’t need to memorise these, but knowing the acronyms can be helpful

- AIFMD – Alternative Investment Fund Managers Directive

- EPD – Environmental Product Declarations

- ESMA – European Securities and Markets Authority

- GHG Protocol – Greenhouse Gas Emission Protocol

- IMM – Impact Managagement Platform

- IPSASB – International Public Sector Standards Board

- MiFID – Markets in Financial Instruments Directive

- SBTN – Science-based Target Network

- SECR – Streamlined Energy and Carbon Reporting

- SFDR – Sustainable Finance Disclosure Regulation

- TNFD – Taskforce on Nature-related Financial Disclosures

- TIFD – Task Force on Inequality-related Financial Disclosures

- UCITS – Undertakings for the Collective Investment in Transferable Securities

- A helpful commentary on these shifts is available via Triodos Investment Management.

Key takeaway

Sustainability, ESG and social value are all part of a larger ecosystem. While they differ in focus, they are increasingly interlinked, and organisations are expected to understand how their work fits into this picture.

Reflection and resources: 10 Impact questions

The Maximise Your Impact guide includes 10 generally agreed impact questions which defined to be asked and answered throughout the different stages of an impact management cycle. The questions, and aligned stages are:

These impact questions were defined by impact management experts in the UK and across Europe converging the list from across impact measurement and management methodologies.

The questions provide a checklist that anyone can use which helps to determine your impact.

There are 3 overarching questions it is important to consider in relation to all of the questions:

- Who should answer them?

- How rigorous do the answers need to be to inform your decisions?

- What assurances do you need that the information is relevant, complete, and accurate before you are able to make those decisions?

Use our helpful word document to fill in your answers.

Need more social value support?

We know that introducing a new platform – especially one tied to strategy, procurement, or compliance – can feel like a big lift. That’s why we offer our social value Impact Bootcamp, led by our resident impact experts. It’s designed for organisations ready to go beyond the basics and embed social value measurement across their operations. Whether you’re a sustainability lead, part of a cross-functional team, or someone driving change from within the bootcamp equips you with the strategy, tools, and confidence to do more, and prove it.